Frequently Asked Questions

The new tax regime introduced under the Income Tax Act, 1961 provides taxpayers with the option to choose between the existing tax regime and a new tax regime with revised tax rates and slabs.

The old tax regime offers various deductions and exemptions, while the new tax regime offers lower tax rates but fewer deductions and exemptions.

Any individual or Hindu Undivided Family (HUF) taxpayer can opt for the new tax regime, provided they forego certain deductions and exemptions available under the old regime.

Yes, taxpayers have the flexibility to switch between the old and new tax regimes every financial year based on their preference and tax planning requirements.

The tax slabs and rates under the new tax regime are as follows:

Up to Rs. 2.5 lakh: Nil

Rs. 2,50,001 to Rs. 5,00,000: 5%

Rs. 5,00,001 to Rs. 7,50,000: 10%

Rs. 7,50,001 to Rs. 10,00,000: 15%

Rs. 10,00,001 to Rs. 12,50,000: 20%

Rs. 12,50,001 to Rs. 15,00,000: 25%

Above Rs. 15,00,000: 30%

Some of the deductions and exemptions not available under the new tax regime include:

- Standard deduction for salaried individuals

- Deductions under Chapter VI-A (e.g., Section 80C, Section 80D, Section 80G, etc.)

- House rent allowance (HRA)

- Leave travel allowance (LTA)

- Interest on housing loan for self-occupied property (Section 24)

- Special allowances under Section 10(14)

Form 26AS is a consolidated tax statement that provides a comprehensive view of all tax-related information such as TDS (Tax Deducted at Source), TCS (Tax Collected at Source), advance tax, and self-assessment tax deposited against your PAN (Permanent Account Number).

Form 26AS contains the following information:

Details of tax deducted at source (TDS) by deductors Details of tax collected at source (TCS) by collectors.

Advance tax and self-assessment tax payments made by the taxpayer.

Refunds received during the financial year.

High-value transactions reported by banks and other financial institutions.

Details of tax demand and pending tax proceedings, if any

Income tax is a tax imposed by the government on individuals and entities based on their income. It is typically calculated as a percentage of income earned during a specific period, such as a calendar year.

Taxpayers in India, including individuals under 60 years of age earning more than Rs.2.5 lakh and those above 60 years of age earning above the same threshold, are obligated to pay income tax under old regime. Resident Individuals are further classified based on age, with those below 60 and those aged 60 to 80 having different tax rules.

If you do not file an Income tax return, you cannot carry forward or set off your losses. Filing of the Income-tax return not only helps you but also helps the nation. The tax that you pay is used by the government to build infrastructure and to improve other facilities of the nation such as medical, defence, etc.

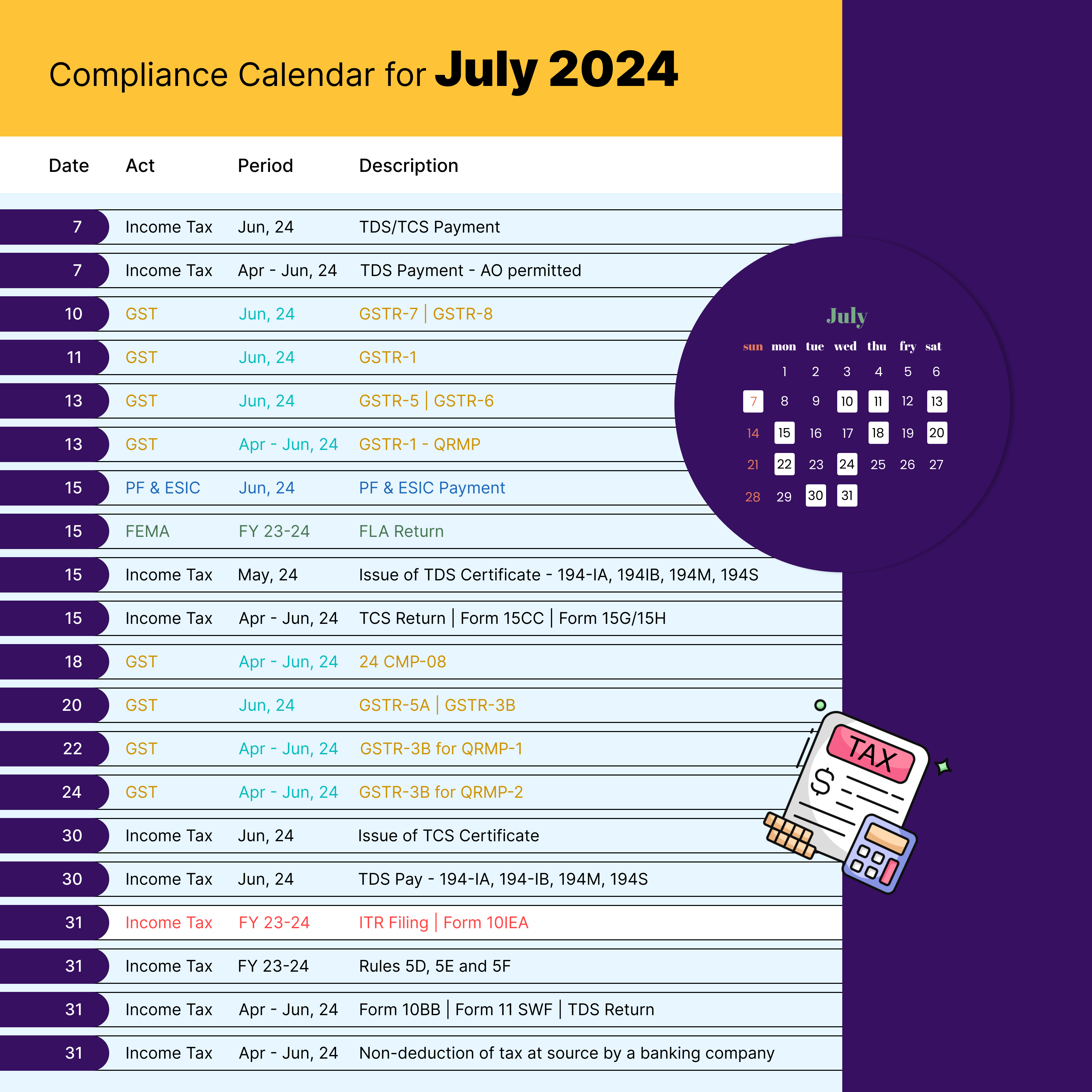

You must file your income tax returns (ITR) for the financial year ending 31st March by 31st July of the same year.

No, there is no need to produce documents at the time of filing your tax return. However, in case there is a scrutiny, you may be required to submit these documents.

- PAN Card

- Aadhaar Card

- Form 16

- Month-wise salary slips Form-16A/ Form-16B/ Form- 16C

- Bank Account Details

- Bank Statement/Passbook

- Investment Proofs (Deductions and investments that can be claimed under section 80C, 80D, 80E, 80TTA, etc.)

- Form 26AS

- Interest Income and Other Interest Certificates

- Capital Gains from Sale of Property, Mutual Funds, Shares

- Details of Investment in Unlisted Shares

- Home Loan Statement

- Rental Income

- Foreign Income/Dividend Income

Taxable income is the portion of your total income that is subject to taxation after deductions and exemptions are applied. It includes wages, salaries, investment income, and other sources of income.

Any year you have minimal or no income, you may be able to skip filing your tax return and the related paperwork. However, it’s perfectly legal to file a tax return showing zero income, and this might be a good idea for a number of reasons

There are 5 Heads of Income as per the Income Tax Act, viz., Income from Salaries, Income from House Property, Income from Profits and Gains from Business and Profession, Income from Capital Gains, and Income from Other Sources.

Income from Other Sources in India refers to the income earned from various sources that do not fall under the other specified heads of income like Salary, House Property, Business/Profession, and Capital Gains. It includes interest income, rental income, dividends, gifts, lottery winnings, and more.

Profits and Gains from Business or Profession A professional could easily arrive at his taxable “Income under the head Profits and Gains from Business or Profession” by reducing all his profession related expenses from this gross receipts out of the profession

Agricultural income covers all land produce such as grain, fruits, commercial crops, etc. However, it does not include using a piece of land for poultry farming, breeding of livestock, dairy farming, and the like.

According to the Income Tax Act of 1961, every salaried person must pay an amount from their salary as tax to the country. This amount of tax is called income tax. The law consists of many provisions and variations with subsections describing the details of tax payments, deductions, and computations.

Tax is one of the main reasons amongst others. Employers deduct tax from your salary before paying it in your account and deposits it with the government on behalf of the employee. This concept of deducting taxes before making the payment is known as TDS: Tax Deduction at Source

Yes, if you have already filed your income tax return manually (offline), you can still E-verify it using any of the available electronic verification methods within the specified time frame.

All types of properties are taxed under the head ‘income from house property’ in the income tax return. An owner for the purpose of income tax is its legal owner, someone who can exercise the rights of the owner in his own right and not on someone else’s behalf.

- Types of house property

- Self-occupied house property.

- Let-out house property.

- Deemed let-out house property.

The annual value of self-occupied property is considered nil. Therefore, a self-occupied house is supposed to be non-revenue generating, hence not taxable.

Income from a business or profession is calculated on the basis of method of accounting regularly employed by the assessee1. If the assessee has adopted mercantile system of accounting, then income is calculated on accrual basis as well as admissible expenses are deducted on accrual basis.

Any income earned by a taxpayer with an intention to earn a profit is covered under the head business and profession. There are 3 types defined for Businesses/profession under the income tax act: Non-Speculative Businesses/Profession: Includes profits/loss from all the normal business carried by a taxpayer.

Capital gain is denoted as the net profit that an investor makes after selling a capital asset exceeding the price of purchase. The entire value earned from selling a capital asset is considered as taxable income.

Rs 1 lakh per year

Capital gains up to Rs 1 lakh per year are exempted from capital gains tax. Long-term capital gain tax rate on equity investments/shares will continue to be charged at 10% on the gains. On the other hand, short-term capital gains tax on shares or equity investments will be charged at 15%.

Income from Other Sources in India refers to the income earned from various sources that do not fall under the other specified heads of income like Salary, House Property, Business/Profession, and Capital Gains. It includes interest income, rental income, dividends, gifts, lottery winnings, and more.

The Income Tax Act allows you to file a belated ITR on any past year before the end of the assessment year or before the end of income checking on that year. For instance, if you failed to file for 2021-22, you have until March 31, 2024, unless the government ends its checks before that.

Any income earned outside India is taxable both in the country where it is accrued and in India. To avoid double taxation, the government has provided the benefit of FTC, wherein the taxpayer can claim a deduction on the tax paid.

Section 139(5) of the Income Tax Act, 1961, allows you to file a revised return if you discover mistakes in your initial filing. You can even revise a belated return. You can file a revised return by 31st December of the relevant assessment year or before the completion of assessment, whichever is earlier.

Yes, you can ITR-U, if you have missed to file your previous two ITRs. For current year you can file your normal ITR.

Presumptive taxation allows you to pay your tax based on presumptive income. Meaning, you don’t really need to estimate your income by deducting your expenses from revenue. You can simply take a percentage of your total revenue and pay tax on that.